I would like to calibrate a interest rate tree using the optimization tool in matlab. Need some guidance on doing it.

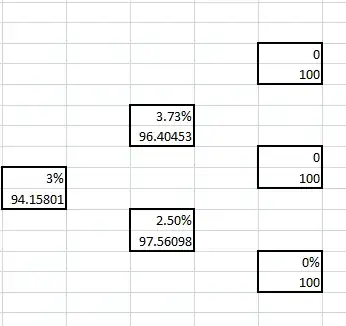

The interest rate tree looks like this:

How it works:

3.73% = 2.5%*exp(2*0.2)

96.40453 = (0.5*100 + 0.5*100)/(1+3.73%)

94.15801 = (0.5*96.40453+ 0.5*97.56098)/(1+2.50%)

The value of 2.5% is arbitrary and the upper node is obtained by multiplying with an exponential of 2*volatility(here it is 20%).

I need to optimize the problem by varying different values for the lower node.

How do I do this optimization in Matlab?

What I have tried so far?

InterestTree{1}(1,1) = 0.03;

size = size(InterestTree,2);

InterestTree{size-1}(1,size-1)= 2.5/100;

InterestTree{size}(2,:) = 100;

InterestTree{size-1}(1,size-2)= (2.5*exp(2*0.2))/100;

InterestTree{size-1}(2,size-1)=(0.5*InterestTree{size}(2,size)+0.5*InterestTree{size}(2,size-1))/(1+InterestTree{size-1}(1,size-1));

j = size-2;

InterestTree{size-1}(2,size-2)=(0.5*InterestTree{size}(2,j+1)+0.5*InterestTree{size}(2,j))/(1+InterestTree{size-1}(1,j));

InterestTree{size-2}(2,size-2)=(0.5*InterestTree{size-1}(2,j+1)+0.5*InterestTree{size-1}(2,j))/(1+InterestTree{size-2}(1,j));

New Edit:

function [ diff ] = InterestTreeComputation(Interest,DiscountedValue,alpha)

total= size(Interest,1);

n = ceil(0.5*(-1+sqrt(1+8*total)));

DiscountedValue(end:-1:(end-n+1)) = 100;

m=0;

for i=total-n:-1:total-2*n+2

Interest(i)= (alpha*exp(2^(m)*0.005))/100;

m = m+1;

end

for j= total-n:-1:1

columnnumber =ceil(0.5*(-1+sqrt(1+8*j)));

DiscountedValue(j) = (0.5*DiscountedValue(j+columnnumber)+0.5*DiscountedValue(j+columnnumber+1))/(1+Interest(j));

end

Data = xlsread('InterestData.xlsx');

ActualValue = Data(:,4);

diff = (DiscountedValue(1) - ActualValue(n-1))^2;

end

How I call it:

clear all;close all;clc;

Interest = [0.0954;0;0];

DiscountedValue =zeros(3,1);

Interest = [Interest; zeros(3,1)];

DiscountedValue = [DiscountedValue; zeros(3,1)];

fhand = @(x)InterestTreeComputation(Interest,DiscountedValue,x);

x0 = 2.5;

x_optimal = fminunc(fhand, x0);

How do you optimize this function? Is it like this => x = fminunc(@ITree,x0)?