Consider a sequence of length $s+m$ with $s$ successes and $m$ failures in total.

You know that the number of such sequences is given by ${{s+m} \choose m} $, and that each has a probability of $p^s (1-p)^{m}$

A sequence as above can be considered a binary string of length $s+m$, with $s$ ones in total.

Now you can refer to the answers to this other post [ number of occurrences of k consecutive 1s in a binary string of length n ]

(http://math.stackexchange.com/questions/2045496)

where it is explained that

the number of binary strings with $s$ 1's, $m$ 0's, and which contains runs of consecutive 1's of length at most $r$ is

given by

$$

N_b (s,r,m + 1) = {\rm No}{\rm .}\,{\rm of}\,{\rm solutions}\,{\rm to}\;\left\{ \matrix{

{\rm 0} \le {\rm integer}\;x_{\,j} \le r \hfill \cr

x_{\,1} + x_{\,2} + \; \cdots \; + x_{\,m + 1} = s \hfill \cr} \right.

$$

where $N_b (s,r,m + 1) $ is expressible by the sum

$$ \bbox[lightyellow] {

N_b (s,r,m + 1)\quad \left| {\;0 \le {\rm integers }s,m,r} \right.\quad = \sum\limits_{\left( {0\, \le } \right)\,\,k\,\,\left( { \le \,{s \over r}\, \le \,m + 1} \right)} {\left( { - 1} \right)^k \left( \matrix{

m + 1 \cr

k \cr} \right)\left( \matrix{

s + m - k\left( {r + 1} \right) \cr

s - k\left( {r + 1} \right) \cr} \right)}

}$$

So we conclude that

the probability of having at most $r$ consecutive successes in $n$ Bernouilli trials,

each with success probability $p$

is given by

$$ \bbox[lightyellow] {

P_{\,M}(r,p,n) = \sum\limits_{0\, \le \,\,s\,\, \le \,n} {p^{\,s} \left( {1 - p} \right)^{\,n - s} \sum\limits_{\left( {0\, \le } \right)\,\,k\,\,\left( { \le \,{s \over r}\, \le \,n - s + 1} \right)} {\left( { - 1} \right)^k \left( \matrix{

n - s + 1 \cr

k \cr} \right)\left( \matrix{

n - k\left( {r + 1} \right) \cr

s - k\left( {r + 1} \right) \cr} \right)} }

}$$

while instead

the probability of having at least $r$ consecutive successes in $n$ Bernouilli trials,

each with success probability $p$

(the one you are looking for) is clearly

$$ \bbox[lightyellow] {

P_{\,L} (r,p,n) = 1 - P_{\,M} (r - 1,p,n)

}$$

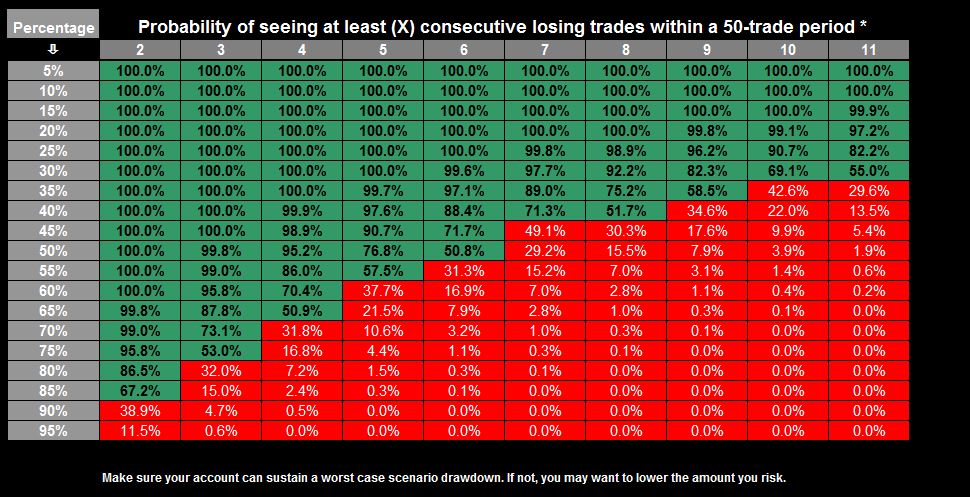

For example, with a win probability of $0.9$ (thus loss $=0.1$) the probability of having at least $2$ consecutive

losses (successes) in $50$ tradings will be

$$

P_{\,L} (2,0.1,50) = 1 - P_{\,M} (1,0.1,50) = 0.36367...

$$

as correctly pointed out by Henry.

Some other values are given in this table (here p = win)

$$

\begin{array}{l}

P_{\,L} (r,\;1 - p,\;50) \\

\begin{array}{c|ccc}

\hline

{p\backslash r} & & 2 & 3 & 4 \\

\hline

{0.3} & & {1.0} & {1.0} & {0.9978} \\

{0.5} & & {1.0} & {0.9827} & {0.8274} \\

{0.8} & & {0.8202} & {0.2707} & {0.059} \\

{0.9} & & {0.3634} & {0.0425} & {0.0042} \\

\end{array} \\

\end{array}

$$

Also, putting $r=2 \; p (win)=0.9$ and $n=0,1,2,..$, it is easy to check that we obtain the values already indicated

by Henry at the end of his answer.

And to satisfy your curiosity, $P_{\,L} (15,\;0.55,\;500) = 0.0275867...$ again confirming Henry's answer.

However, for large $n$ an asymptotical formula would be needed, which at the moment I did not succeed and find.

calc_prob(n_trades=20000, x_loses=13, probability=0.4). def calc_prob(n_trades, x_loses, probability): # Initial values gn = [1] fn = 0 for trade in range(1, n_trades + 1): # Calculate actual G(n) g_num = trade - x_loses gna = probability * (1 - fn) gn.append(gna) gna = gn[g_num] if g_num >=0 else 0 # Calculate actual F(n) fn = fn + ((1 - probability)*x_loses) float(gna) ret – Michal Gow Feb 15 '19 at 12:16