Assume that $f_Y$, the pdf of $Y\ge 0$, exists. In this case the expected value is

$$E[Y]=\int_{0}^{+\infty}x\ f_Y(x)\ dx$$

Also, assume that the integral above is finite.

It is obvious that $x$ can be written as

$$x=\int_0^x\ 1\ dy, \ x\ge 0.$$

With this, the expected value is

$$E[Y]=\int_{0}^{+\infty}\int_0^x\ 1\ dy\ f_Y(x)\ dx.$$

Since the expectation exists we can use Fubini' theorem so we can compute this integral as a double integral.

$$E[Y]=\iint_A1\cdot d\mu(x,y)$$

where

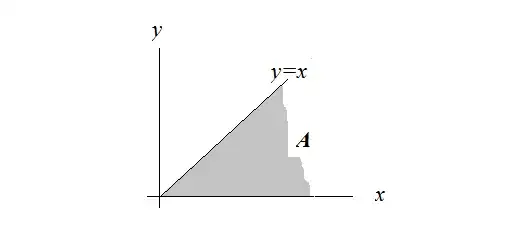

$$A=\{(x,y): 0\le y\le x\ \text{ and } 0 \le x < \infty \}.$$

and $\mu$ is the product measure of the probability measure generated by $f_Y$ and the Lebesgue measure. (For a rectangle $r=[a,b]\times [c,d]$, the measure $\mu(r)=(b-a)\int_c^df_Y(x)\ dx$.)

The domain of the integration can be visualized:

Considering the definition of $\mu$ and the shape of the domain, and referring to Fubini's theorem, the double integral above can be written as

$$\int_{0}^{+\infty}\int_{y}^{+\infty}\ 1\ f_Y(x)\ dx\ dy=$$

$$=\int_{0}^{+\infty}P(Y\ge y)\ dy.$$